How Sale-Leasebacks Work: A Profit Example

May 2, 2014 | Posted In Insider's View, News & Resources, Newsletters

By: Carrie S. Holstead – President & CEO, Carrie S. Holstead Real Estate Consultants, Inc. / ITRA Global Pittsburgh & Vice Chairman of the Board, ITRA Global

The basic premise of a Sale-Leaseback is that the income stream generated by a multi-million dollar asset has more value than the cost of the asset without an income stream. Sale-Leasebacks can be used to unlock capital from existing assets or to fund projects of all sorts (please contact us for a partial list), using the same basic methodology as described below. As importantly, the seller maintains operational control of the property as if it were still owned by the tenant company.

By way of example, let’s say a private or public sector organization needs a new building (or owns an existing building) of approximately 150,000 square feet and is willing to sign a 15 year lease.

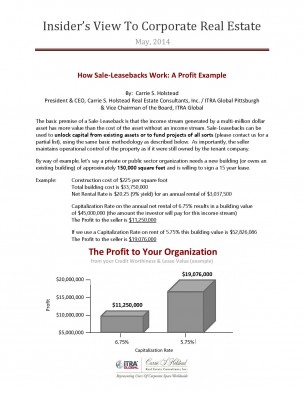

Example:

Construction cost of $225 per square foot

Total building cost is $33,750,000

Net Rental Rate is $20.25 (9% yield) for an annual rental of $3,037,500

Capitalization Rate on the annual net rental of 6.75% results in a building value of $45,000,000 (the amount the investor will pay for this income stream) The Profit to the seller is $11,250,000

If we use a Capitalization Rate on rent of 5.75% this building value is $52,826,086

The Profit to the seller is $19,076,000